How I Navigated a Debt Crisis Using Smart Tax Strategies

Facing a debt crisis felt like drowning—until I discovered how tax strategy could change everything. It wasn’t about hiding money or exploiting loopholes, but using legitimate financial tools smarter. I restructured my obligations, turned deductions into breathing room, and recovered faster than I thought possible. This is how I did it—and how you might too, if you're in the same boat.

The Breaking Point: When Debt Overwhelmed Me

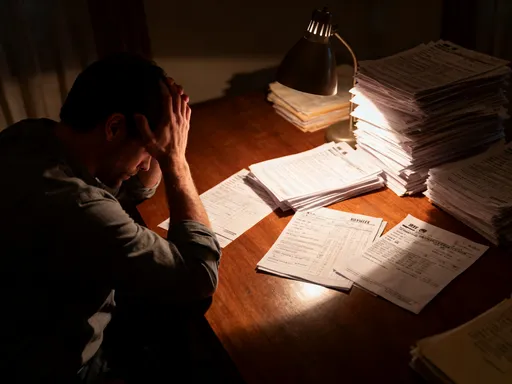

There was a time when opening the mailbox filled me with dread. Every envelope seemed to carry another bill, another reminder of how far behind I had fallen. Credit card statements, medical bills, and a personal loan I took out during a lean year had snowballed into a total I could no longer ignore—over $47,000 in unsecured debt. My monthly payments consumed nearly 40% of my take-home pay, leaving little for groceries, utilities, or unexpected expenses. I was working full time, living frugally, and yet each month ended with a sinking feeling that I was running in place.

The emotional toll was just as heavy as the financial burden. I lost sleep, worried about phone calls from creditors, and felt a constant sense of shame. I avoided checking my credit report and stopped talking about money, even with close friends. The idea of financial freedom felt like a fantasy. I tried traditional debt repayment methods—listing all my balances, prioritizing high-interest cards, and even transferring balances to lower-rate cards—but progress was slow. Each small payment barely made a dent, and when emergencies arose, I had no cushion. I realized that cutting expenses alone wasn’t enough. I needed a different kind of leverage, one that could generate breathing room not just through spending less, but through earning and retaining more of what I already had.

That’s when I began to look beyond budgeting and consider how the tax system might offer unexpected relief. I had always treated taxes as a fixed cost—an annual obligation with little room for influence. But as I dug deeper, I discovered that tax strategy wasn’t just for accountants or the wealthy. For someone in crisis, it could be a lifeline. With professional guidance, I began to see how legal, well-timed decisions around income, deductions, and debt forgiveness could reduce my liabilities and free up cash exactly when I needed it most. This wasn’t about gaming the system; it was about understanding it well enough to survive it—and eventually, thrive within it.

The Hidden Lever: Why Tax Strategy Matters in a Crisis

Most people think of taxes as something to endure, not something to manage proactively—especially during a financial crisis. When you’re overwhelmed by debt, the last thing on your mind might be your W-2 or estimated tax payments. But I learned that tax planning isn’t just about April 15th; it’s a year-round financial lever that, when pulled wisely, can ease pressure, improve cash flow, and even prevent further debt accumulation. The key shift for me was realizing that taxes are not a fixed expense but a variable one—something I could influence through timing, structure, and informed decisions.

For example, lowering your taxable income doesn’t just reduce what you owe to the IRS—it increases the amount of money you can keep and use to pay down debt. A $5,000 reduction in taxable income might save you $1,000 to $1,500 in taxes, depending on your bracket. That’s real money that can go toward your credit card balance or medical bill. Similarly, understanding how different types of income are taxed—such as earned income versus investment income—can help you make smarter choices about when to accept payments or withdraw from accounts. These aren’t loopholes; they’re features of the tax code designed to encourage certain behaviors, like saving for retirement or investing in health.

What made the biggest difference for me was moving from a reactive to a strategic mindset. Instead of waiting for tax season and reacting to what had already happened, I started planning ahead. I met with a tax professional early in the year to project my income, estimate my liabilities, and identify opportunities to reduce my burden. This allowed me to adjust my withholding, defer income, and accelerate deductions—all legal moves that shifted cash flow in my favor. I also learned that some financial decisions have both immediate and tax-related consequences. For instance, paying off a loan early might feel good, but if it means draining an emergency fund, it could leave you vulnerable to future tax bills or unexpected expenses. Strategic tax thinking helped me balance short-term survival with long-term stability.

Restructuring Income: Timing Is Everything

One of the first strategic moves I made was to restructure when I recognized income. I worked as a freelance consultant, which gave me some control over when I invoiced clients and when I received payments. I realized that by deferring certain invoices from December to January, I could push that income into the next tax year—buying myself a full 12 months of delay. This wasn’t about hiding income; it was about lawful timing. That shift alone reduced my taxable income for a critical year by nearly $8,000, which lowered my tax bill and kept more cash in my pocket when I needed it most.

I also negotiated with my part-time employer to delay a year-end bonus from December to January. While it meant waiting a few extra weeks, the tax benefit was significant. By moving that $6,000 bonus into the next calendar year, I avoided being pushed into a higher tax bracket and reduced my marginal tax rate for the current year. This kind of income deferral is completely legal and available to many workers, especially those with flexible compensation arrangements. Even employees who don’t have control over their paychecks can explore options like delaying contributions to non-essential retirement accounts or adjusting withholding if they expect a lower income in the coming year.

Another important step was managing my retirement contributions more deliberately. In previous years, I had maxed out my 401(k) contributions automatically, which reduced my taxable income—but during my debt crisis, I temporarily lowered my contribution rate. This increased my take-home pay slightly, giving me more room to manage monthly obligations. I didn’t stop saving entirely, but I adjusted the pace to match my reality. Once my debt was under control, I gradually increased my contributions again. The lesson was clear: tax-advantaged accounts are powerful, but they should serve your broader financial health, not work against it during a crisis.

Maximizing Deductions: From Wasteful to Strategic Spending

As I worked to reduce my tax burden, I began to see everyday expenses in a new light. Things I once viewed as unavoidable costs—medical bills, home improvements, charitable donations—could become tools for tax savings if timed and documented correctly. The key was shifting from passive spending to intentional, tax-aware decisions. I didn’t spend more; I spent smarter. By aligning necessary expenses with tax planning, I turned deductions into a form of financial relief.

One of the most impactful changes was in how I handled medical expenses. I had always paid doctor visits, prescriptions, and insurance premiums without thinking about tax implications. But I learned that medical expenses above 7.5% of adjusted gross income (AGI) are deductible if I itemize. In a year when I had several procedures and ongoing treatments, my total medical costs reached over $9,000. With my AGI around $58,000, the threshold was about $4,300—meaning I could deduct nearly $4,700. That translated into hundreds of dollars in tax savings. More importantly, it encouraged me to schedule certain non-urgent procedures in the same year to maximize the deduction, rather than spreading them out and losing the benefit.

I also set up a home office, which allowed me to claim the home office deduction. Since I worked remotely several days a week, a portion of my rent, utilities, and internet became deductible. I didn’t renovate or buy expensive equipment—I simply designated a corner of my living room as my workspace and kept detailed records. The deduction wasn’t huge—around $1,200—but every dollar counted. I also began tracking mileage for business-related travel and kept receipts for all work supplies. These small deductions added up and reinforced a mindset of financial awareness.

Charitable giving became another strategic tool. Instead of donating randomly throughout the year, I bundled donations into a single tax year to exceed the standard deduction threshold. In one year, I donated $8,000 to a local food bank and educational nonprofit, all documented with receipts. By itemizing, I gained a deduction that reduced my taxable income significantly. I didn’t give more than I could afford—but I gave in a way that aligned with both my values and my financial strategy. This approach, sometimes called “bunching” deductions, is a legal and effective way to maximize tax benefits without increasing spending.

Debt Relief and Tax Consequences: What Few Understand

One of the most surprising lessons I learned was that debt relief can come with a tax cost. After negotiating with one of my creditors, I managed to settle a $12,000 credit card balance for $6,000. I felt a wave of relief—until I received a Form 1099-C the following January, showing $6,000 of canceled debt as taxable income. That meant I might owe taxes on money I never actually received. For someone already struggling, this could have been a devastating blow. A $6,000 increase in taxable income could mean an extra $1,000 to $1,800 in taxes, depending on the bracket. I was stunned—how could being forgiven a debt result in a new tax bill?

After consulting a tax professional, I discovered an important exception: the insolvency exclusion. If you are insolvent when debt is canceled—meaning your total liabilities exceed your total assets—you can exclude the canceled debt from taxable income. I qualified. At the time of the settlement, my debts far outweighed my assets, including my car, savings, and personal property. By completing IRS Form 982 and attaching it to my return, I was able to exclude the $6,000 from my income and avoid the tax liability. This was a turning point. It taught me that tax rules aren’t always intuitive, and that understanding exceptions can make the difference between recovery and setback.

I also learned that not all forgiven debt is treated the same. Mortgage debt forgiven under certain federal programs, for example, may be excluded under the Mortgage Forgiveness Debt Relief Act (though this applied only to specific years and circumstances). Student loan forgiveness may have tax implications unless covered by a tax-free provision, such as under the Public Service Loan Forgiveness program. The lesson was clear: before accepting any debt settlement, it’s essential to understand the tax consequences. A lower balance today could mean a higher tax bill tomorrow—unless you plan for it.

Building Safeguards: Tax Planning as Risk Control

Once I had stabilized my finances and paid off the worst of my debt, I shifted from survival to sustainability. I knew that without safeguards, I could easily fall back into the same cycle. That’s when I turned tax-advantaged accounts into tools for long-term protection. I began contributing to a Roth IRA, not just for retirement, but as a flexible savings vehicle. Contributions can be withdrawn at any time without tax or penalty, making it a reliable emergency fund in addition to a retirement account. I started with small amounts—$100 a month—but consistency mattered more than size.

I also opened a Health Savings Account (HSA) after switching to a high-deductible health plan. The triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses—made it one of the most powerful tools I discovered. I used it to pay for prescriptions, doctor visits, and future health needs, while also allowing the balance to grow over time. Unlike flexible spending accounts (FSAs), HSAs don’t have a use-it-or-lose-it rule, so the money rolls over year after year. By funding it strategically—using tax refunds or bonus income—I built a health reserve that also reduced my taxable income.

At the same time, I rebuilt my emergency fund, this time with tax implications in mind. I kept it in a high-yield savings account, which generated modest interest. While that interest is taxable, it’s minimal and the liquidity was worth it. I avoided riskier investments for this fund, knowing I might need the money quickly. I also reviewed my withholding annually to ensure I wasn’t overpaying the IRS and giving the government an interest-free loan. By adjusting my W-4 form, I increased my take-home pay slightly, which I directed straight into savings. These steps didn’t make me rich overnight, but they created a buffer that prevented future crises.

Lessons from the Edge: What Truly Works Under Pressure

Looking back, no single decision saved me. It was the combination of awareness, discipline, and professional guidance that made the difference. I learned that tax strategy isn’t a luxury for the wealthy—it’s a practical, accessible tool for anyone facing financial hardship. You don’t need to be a CPA to benefit from smarter tax planning, but you do need to be informed and proactive. The most powerful moves I made were simple: timing income, maximizing deductions, understanding debt forgiveness rules, and using tax-advantaged accounts to rebuild.

Patience was essential. Recovery didn’t happen in a month or even a year. It took three years of consistent effort, careful planning, and occasional setbacks. But each small win—avoiding a tax bill, reducing a liability, building a cushion—added up. I also learned the value of professional advice. A fee-only financial planner and a licensed tax preparer helped me navigate complex rules and avoid costly mistakes. Their fees were an investment, not an expense.

Today, I’m debt-free, financially stable, and more confident than ever. I still file my taxes early, review my strategy annually, and teach others what I’ve learned. The experience transformed my relationship with money. I no longer see taxes as an enemy, but as a system I can work within to protect my future. If you’re in a debt crisis, know this: you’re not alone, and there is hope. With the right mindset and tools, recovery is possible. And sometimes, the quietest lever—smart tax planning—can be the one that lifts you out of the deepest hole.