How I Mastered My Money in Retirement Communities — Real Financial Skills That Work

What if your retirement community could be more than just a place to live — but a smart hub for growing your financial confidence? I moved in a few years ago thinking it was just about comfort, but quickly realized managing money here takes real skill. From unexpected fees to social spending traps, I’ve learned what protects your nest egg and what drains it fast — and I’m sharing it all. This isn’t about cutting corners or living frugally; it’s about making informed choices that preserve your independence and peace of mind. The truth is, financial stability in retirement communities doesn’t come from how much you have — it comes from how well you manage what you’ve worked so hard to save.

Why Retirement Communities Come with Hidden Financial Traps

Retirement communities are often marketed as worry-free havens, where maintenance, meals, and activities are all taken care of. While that promise holds some truth, the reality is more complex. These communities operate like small towns with their own financial systems, and many residents enter without fully understanding the economic landscape they’re stepping into. The initial appeal of a simplified lifestyle can quickly fade when unanticipated charges begin to appear on monthly statements. These aren’t necessarily signs of dishonesty, but rather the result of fine print, evolving service models, and assumptions that can be easy to overlook during the excitement of moving in.

One of the most common surprises involves what’s known as the “bundled fee” model. On the surface, a single monthly payment seems straightforward — it covers housing, utilities, basic upkeep, and access to amenities. However, what many don’t realize is that these bundles often exclude a range of services that become essential over time. For example, assistance with daily tasks such as medication management or help with bathing may not be included unless you upgrade to a higher care level, which comes with a significantly increased cost. Similarly, home modifications for mobility — like installing grab bars or widening doorways — are rarely covered and can cost thousands when billed separately.

I learned this lesson after my first winter here. A minor fall led to a recommendation for additional safety checks in my unit. When I requested a grab bar installation, I was quoted $420 — not covered by my monthly fee. That moment was a wake-up call. It wasn’t just about the cost of one fixture; it was about recognizing that even small needs could lead to unplanned expenses. Other residents have shared similar experiences: unexpected charges for guest parking, pet fees that increase annually, or even fines for late meal cancellations. These may seem minor in isolation, but over time, they accumulate and strain even well-planned budgets.

The deeper issue lies in how these communities structure their contracts. Sales materials often emphasize convenience and lifestyle, while the financial details are buried in lengthy agreements that few read thoroughly before signing. This isn’t unique to retirement living — it’s a pattern seen in many service-based industries — but the stakes are higher here because residents are typically older, on fixed incomes, and less likely to switch providers. That makes transparency especially important. Understanding the full scope of potential costs before moving in — including escalation clauses that allow fees to rise annually — is critical. It’s not about fearmongering; it’s about empowerment through awareness.

The Truth About Monthly Fees: What They Cover (and What They Don’t)

At first glance, the monthly fee in a retirement community appears to be a simple, all-inclusive payment — similar to a rent or subscription model. Residents pay a set amount each month, and in return, they receive housing, meals, housekeeping, transportation, and access to social and wellness programs. This simplicity is part of the appeal, especially for those who want to reduce the mental load of managing multiple bills. But beneath this streamlined surface lies a more nuanced reality. Many of the services that seem included are actually tiered, with basic access provided at one level and enhanced or specialized services requiring additional fees.

Take dining, for instance. Most communities offer a certain number of meals per week in the main dining hall as part of the base fee. That sounds generous — until you realize that specialty dinners, holiday feasts, or guest meals often come with surcharges. I once attended a Thanksgiving dinner with a visiting niece and was surprised to see a $38 charge on my next bill. It wasn’t hidden, but it wasn’t clearly explained during the tour either. Similarly, some communities offer “flex dining” plans where unused meals roll over, while others operate on a use-it-or-lose-it basis. Not knowing the difference can lead to either wasted benefits or unexpected costs.

Another area of confusion is fitness and wellness programming. While gym access is typically included, group classes — such as yoga, water aerobics, or personal training — are frequently billed separately. I assumed my membership covered all activities, only to find that the popular tai chi class I joined had a $15 per session fee. Over a month, that added up to nearly $60 — not a huge amount, but part of a larger pattern of incremental spending that can catch retirees off guard. Transportation services follow a similar model: basic shuttle rides to medical appointments may be free, but trips to shopping centers, airports, or social events often carry a fee per ride.

The solution isn’t to avoid these services altogether, but to understand them fully before committing. When evaluating a community, ask for a complete itemization of what’s included and what’s considered an extra. Request examples of real resident bills from someone with a similar lifestyle to yours. Track how fees have changed over the past five years — most communities increase rates annually, sometimes by as much as 4% to 6%, which can significantly impact long-term affordability. By treating the monthly fee not as a fixed cost but as a starting point, you gain the clarity needed to plan realistically and avoid budget shortfalls down the road.

Building a Real Budget That Works Inside the Community

A retirement budget built for independent living often falls short once you move into a community setting. Why? Because the spending dynamics shift. In a private home, expenses are more predictable: mortgage or rent, utilities, groceries, insurance, and occasional repairs. In a retirement community, many of those are absorbed into the monthly fee, but new categories emerge — particularly around lifestyle and social engagement. These aren’t luxuries; they’re essential to emotional well-being. But they can also become financial leaks if not managed intentionally.

One of the biggest challenges is what financial planners call “lifestyle creep” — the gradual increase in spending that happens when new conveniences become habits. It starts small: “I’ll just have lunch at the dining hall today.” Then it becomes, “Everyone’s going to the wine tasting — I should join.” Before long, you’re spending $400 a month on meals and events without realizing it. I fell into this trap during my first year. I wanted to be social, to feel connected, and the easiest way to do that was to say yes. But when I reviewed my spending at the end of the year, I saw that I’d spent over $5,000 on dining and activities — more than I’d allocated for travel.

That experience led me to rebuild my budget with greater precision. I started by categorizing my spending into three buckets: essentials, lifestyle, and discretionary. Essentials include the monthly fee, insurance, medications, and personal care. Lifestyle covers regular social spending — meals out, classes, outings — while discretionary is for one-time events like trips or gifts. I set a weekly limit for the lifestyle category, treating it like a paycheck I couldn’t exceed. This wasn’t about cutting back on joy; it was about making choices with intention. If I wanted to attend a $75 dinner event, I knew I’d need to scale back elsewhere that week.

I also began tracking every expense manually for three months, using a simple spreadsheet. This helped me identify patterns — for example, I noticed I spent more on weekends when friends visited, and less during quieter weeks. With that data, I adjusted my allocations to reflect real behavior, not idealized plans. The goal wasn’t austerity; it was sustainability. By aligning my spending with my values — connection, health, independence — I gained confidence that I could enjoy life without jeopardizing my financial security.

Smart Ways to Protect Your Income from Inflation and Fees

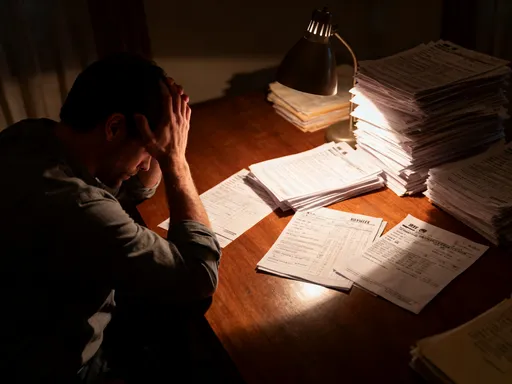

Retirement income is often designed to be stable — Social Security, pensions, annuities, and investment withdrawals provide a predictable flow of funds. But stability doesn’t mean immunity. Over time, inflation erodes purchasing power, and rising fees in retirement communities can outpace income growth. I’ve seen neighbors who entered with comfortable budgets now struggling to keep up, not because they overspent, but because their fixed payments haven’t kept pace with annual fee increases. This is one of the most underdiscussed risks in retirement planning: the gap between static income and rising living costs.

The most effective defense is income diversification. Relying solely on Social Security or a pension leaves little room for error when expenses rise. Adding even one or two supplemental income streams can create a crucial buffer. For some, that means generating rental income from a former home or investment property. For others, it could involve dividend-paying stocks or low-risk bond funds that provide quarterly payouts. I’ve also known residents who use their expertise to do light consulting — a retired accountant preparing taxes in season, or a former teacher offering tutoring. These aren’t about building wealth; they’re about maintaining balance.

Equally important is regular portfolio review. Many retirees set up their investment mix once and rarely revisit it. But as you age, your risk tolerance and financial needs change. A portfolio heavy in growth stocks may have made sense at 65, but at 75, with rising healthcare and care needs, a more conservative, income-focused approach may be wiser. Working with a financial professional to rebalance every few years ensures your assets continue to serve your current reality, not just your past goals.

Another strategy is to build a “fee reserve” — a dedicated savings account set aside specifically for unexpected or rising costs. I started mine with $2,000 and now contribute $100 a month. It’s not meant to cover major medical expenses — that’s what insurance is for — but for things like special assessments, one-time upgrades, or temporary care boosts. Having this fund has given me peace of mind, knowing I won’t have to dip into long-term savings or reduce my standard of living when costs rise.

Avoiding Social Spending Traps and Peer Pressure

Social life is one of the greatest benefits of living in a retirement community. The friendships, shared meals, group outings, and events contribute significantly to emotional and mental well-being. But with that richness comes financial pressure. When everyone around you is signing up for the cruise, joining the art class, or hosting a themed dinner, it’s easy to feel obligated to participate — even when it doesn’t fit your budget. The desire to belong, to stay engaged, can override financial caution. I know this firsthand. In my early months here, I said yes to nearly every invitation, not because I could afford it, but because I didn’t want to feel left out.

Over time, I realized that my social spending was exceeding my grocery budget — a clear sign of imbalance. The turning point came when I reviewed my bank statements and saw how much I’d spent on optional events: $65 for a winery tour, $50 for a holiday gala, $30 for a guest speaker dinner. Individually, each seemed reasonable. Together, they totaled over $800 in three months — money that could have gone toward a future trip or emergency fund. I wasn’t living lavishly; I was just trying to connect. But the cost was real.

My solution wasn’t to withdraw from social life, but to plan for it. I began marking the community calendar each month, identifying which events truly mattered to me — those aligned with my interests or relationships — and which were just convenient distractions. I set a monthly entertainment budget and stuck to it. If I wanted to attend a high-cost event, I planned ahead by reducing spending elsewhere. I also started hosting low-cost gatherings at home — coffee mornings, game nights — which allowed me to socialize without the markup of community fees.

Saying no became easier once I reframed it. It wasn’t about missing out; it was about choosing wisely. I learned to respond with, “That sounds wonderful — I’ll check my schedule and let you know,” giving myself space to decide without pressure. Most importantly, I realized that true connection doesn’t depend on spending. Some of my deepest conversations have happened on a bench in the garden, not at a $75 dinner. By aligning my social spending with my values, I’ve maintained relationships without compromising my financial health.

Working with Financial Advisors Who Understand Community Living

Not all financial advisors are equipped to guide retirees living in communities. Many operate with a traditional framework — sell the house, downsize to a condo, invest the proceeds — without accounting for the ongoing, service-based economy of retirement communities. I learned this the hard way after hiring an advisor who dismissed my concerns about rising fees as “minor line items.” He didn’t understand that a 5% annual increase on a $4,000 monthly fee translates to an extra $2,400 per year — a significant sum on a fixed income. His advice was based on portfolio returns, not real-life cash flow.

The right advisor should grasp the full financial picture: entrance fees, monthly charges, care level transitions, inflation risks, and lifestyle costs. They should be familiar with the contractual structures of continuing care retirement communities (CCRCs) and how financial guarantees — such as life-care contracts — impact long-term planning. They should also understand the emotional and social dimensions of spending, not just the numbers. When I found a new advisor with experience in senior living finance, the difference was immediate. She asked about my community’s fee history, reviewed my service agreement, and helped me model future cost scenarios based on potential care needs.

She also emphasized the importance of liquidity. In a community setting, unexpected costs can arise quickly — a move to assisted living, a special assessment, or a home modification. Having accessible funds is critical. She recommended keeping 12 to 18 months of community fees in a high-yield savings or money market account, separate from long-term investments. This buffer ensures that short-term needs don’t force the sale of assets at an inopportune time.

When choosing an advisor, ask specific questions: Have you worked with residents in continuing care communities? How do you factor in rising fees and care transitions? Can you help me create a spending plan that includes lifestyle costs? Look for credentials like CFP (Certified Financial Planner) and experience in elder financial planning. The goal is not just investment growth, but sustainable, stress-free living.

Planning Ahead: How to Keep Control as Needs Change

Financial planning in retirement isn’t a one-time event; it’s an ongoing process. As health, mobility, and care needs evolve, so must your financial strategy. One of the most significant transitions occurs when moving from independent living to assisted living or memory care within the same community. While this continuity offers comfort, it also brings new financial realities: higher monthly fees, additional service charges, and sometimes a new entrance fee. I’ve seen residents unprepared for this shift, forced to draw heavily on savings or restructure their estate plans under pressure.

To avoid that, I started preparing early. I set aside a “transition fund” — a dedicated savings account I contribute to monthly. It’s not meant to cover all future care costs, but to smooth the initial jump in expenses. I also reviewed my community’s fee schedule for higher care levels, so I know what to expect. Some communities offer rate locks or phased increases, which can help with planning. Others charge a full premium from day one of the transition. Knowing these details in advance allows for better decision-making.

I’ve also updated my legal and financial documents to reflect potential changes. This includes durable powers of attorney, advance directives, and clear instructions for managing my accounts if I’m no longer able to. I’ve had open conversations with my family about my wishes, so there’s no confusion later. Financial control isn’t just about money; it’s about autonomy. By planning ahead, I ensure that I remain the decision-maker in my life, not just a recipient of services.

The goal isn’t to predict every twist and turn, but to build flexibility into the system. That means having accessible funds, a clear understanding of costs, and a support network that includes both family and professionals. It means revisiting your budget, your investments, and your goals regularly. Retirement communities offer comfort and connection, but the real advantage lies in the opportunity to refine your financial skills in a supportive environment. With awareness, preparation, and intention, you can enjoy the life you’ve earned — with confidence, dignity, and lasting control.

Conclusion

Living in a retirement community offers comfort, connection, and convenience — but without strong financial skills, it can also bring stress and surprise expenses. The real advantage isn’t just the safety of a maintenance-free home or the joy of shared activities; it’s the chance to refine how you manage money in a structured yet dynamic environment. Financial stability here doesn’t come from how much you saved over a lifetime, but from how wisely you use what you have. By staying aware of hidden costs, understanding fee structures, building realistic budgets, and planning for change, you protect not just your nest egg, but your independence. The goal is not to live with fear or restriction, but with intention and clarity. With the right knowledge and habits, you can enjoy the lifestyle you’ve earned — fully, freely, and without losing control of your future.